ENG

REPORT

THE ARTICLE PREPARED UNDER THE SPONSORSHIP OF USAID'S FINANCIAL SECTOR TRANSFORMATION PROJECT

WHAT DOES THAT MEAN?

WHAT DOES THAT MEAN?

Ukrainian FinTech

and Banks Survey 2019

ENG

REPORT

Ukrainian FinTech and Banks Survey 2019

THE ARTICLE PREPARED UNDER THE SPONSORSHIP OF USAID'S FINANCIAL SECTOR TRANSFORMATION PROJECT

WHAT DOES THAT MEAN?

WHAT DOES THAT MEAN?

Journalists of AIN.UA prepared this article following editorial standards and published it under the sponsorship of an advertiser

The key survey findings provided below are a summary of the full Ukrainian FinTech and Banks Survey 2019 report, which may be downloaded from the website of the USAID Financial Sector Transformation project and EY in Ukraine.

Number of respondents

The Ukrainian Fintech Catalog 2019, a product of the Ukrainian Association of Fintech and Innovation Companies, compiled with the support of the National Bank of Ukraine and Visa, presented in August 2019, lists more than 100 companies as participants of the Ukrainian FinTech market. Based on the methodology we have employed, we have approached 88 companies and projects. 41 companies/projects have successfully completed the survey.

The National Bank of Ukraine listed 76 active banks as of 01.10.2019. We have been able to reach 44 banks out of 76 in regards to completing the survey – however, just 14 have successfully completed the survey.

The National Bank of Ukraine listed 76 active banks as of 01.10.2019. We have been able to reach 44 banks out of 76 in regards to completing the survey – however, just 14 have successfully completed the survey.

KEY FINDINGS – FINTECH RESPONDENTS

Profiling

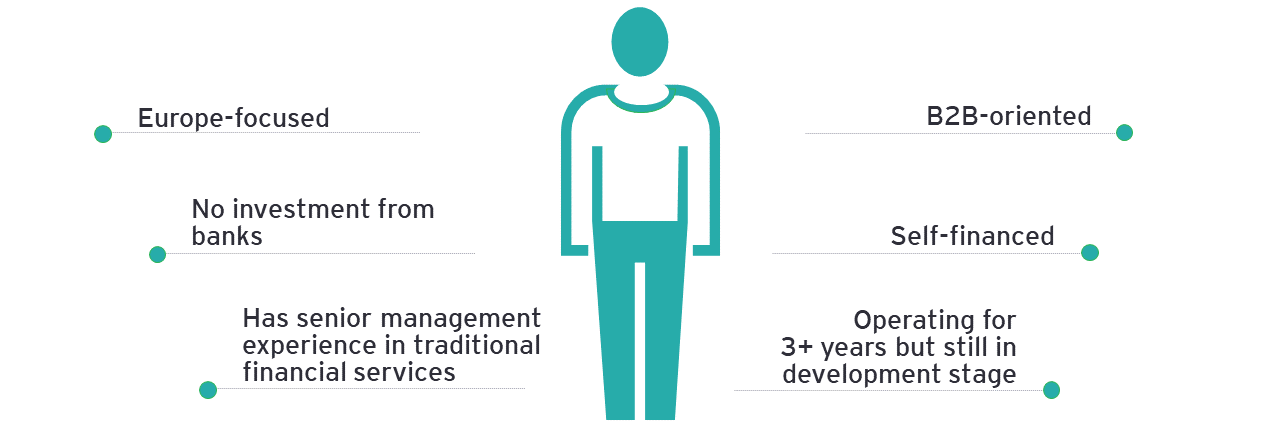

Based on the responses we received, we compiled a summary profile of an average FinTech respondent. The average respondent has been operating for over 3 years but is still developing its product or service. It is fully self-financed, focused on the corporate client market, with top executives experienced in financial services, and not affiliated with banks or banking groups. More often than not, it has expanded beyond Ukraine's borders – and its operations are focused predominantly on the European market.

Average FinTech respondent profile:

Average FinTech respondent profile:

The numbers:

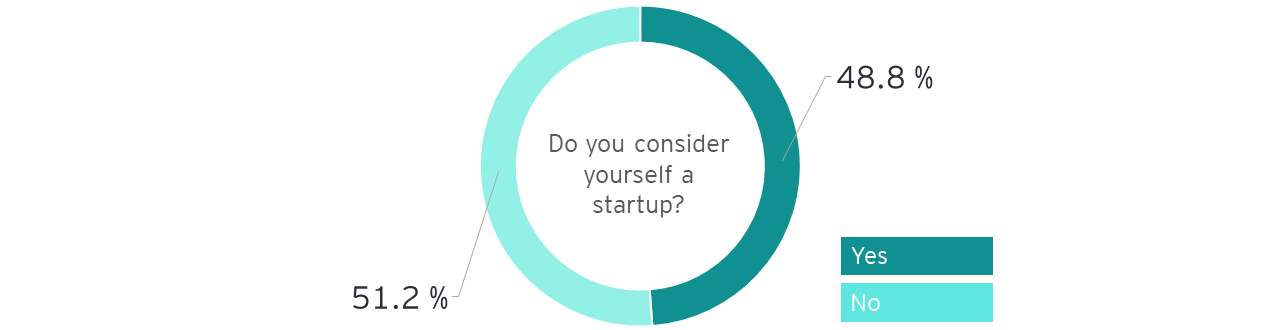

48.8% of the respondents consider themselves a startup. This is somewhat surprising considering revenue generation is a pre-requisite for inclusion into the survey participant list and poses questions as to the definition of a startup by the Ukrainian market participants. At that, 55% of those who consider themselves a startup, have been operating for over 3 years.

75.6% of the respondents have someone in their top management/Board with multi-year expertise in traditional financial services market.

In addition to Ukraine, more than 50% of the companies are operating in the EU (with just close to 20% doing business in non-EU European destinations), with 40+% operating in the CIS region and about 25% in US/Canada and Asian markets, respectively.

41.5% of the respondents operate in Ukraine only.

75.6% of the respondents have someone in their top management/Board with multi-year expertise in traditional financial services market.

In addition to Ukraine, more than 50% of the companies are operating in the EU (with just close to 20% doing business in non-EU European destinations), with 40+% operating in the CIS region and about 25% in US/Canada and Asian markets, respectively.

41.5% of the respondents operate in Ukraine only.

87.8% of the respondents provide B2B services or products. This runs contrary to the global FinTech adoption trends, where corporate adoption lags significantly behind consumer adoption.

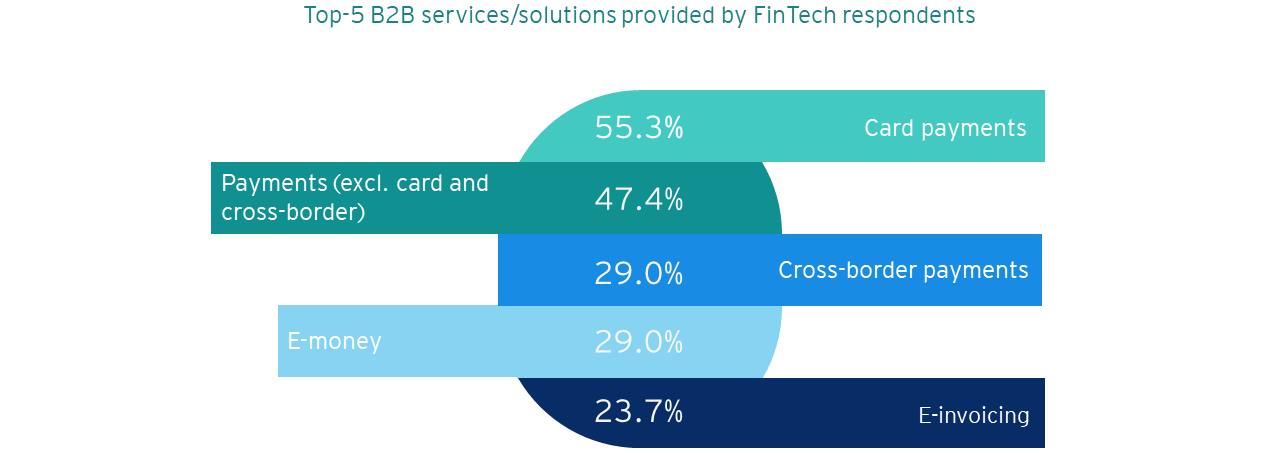

At that, when asked to detail specific services or products they provide, 65.9% were found to be multi-modal (offering both B2B and B2C services/solutions). Across both business models, the two most popular services were card payments and other payment types (excl. card and cross-border payments). Other services consistently present under both business models were e-invoicing and e-money.

The least popular FinTech offerings were found to be treasury services and asset and investment management services. Each of those is provided by one respondent only.

We attribute the abundance of B2B projects to a number of factors, including 1) weak disposable household income dynamics in Ukraine that limit growth potential for B2C-oriented organizations, 2) lack of financial sector infrastructure, especially in the smaller towns and villages and 3) "trust crisis" by the Ukrainians to financial services following liquidations of a large number of banks. Development of B2C solutions also requires significant investments into wide-scale marketing compared to B2B offerings, which the majority of the FinTech projects typically cannot afford given the overall lack of capital.

At that, when asked to detail specific services or products they provide, 65.9% were found to be multi-modal (offering both B2B and B2C services/solutions). Across both business models, the two most popular services were card payments and other payment types (excl. card and cross-border payments). Other services consistently present under both business models were e-invoicing and e-money.

The least popular FinTech offerings were found to be treasury services and asset and investment management services. Each of those is provided by one respondent only.

We attribute the abundance of B2B projects to a number of factors, including 1) weak disposable household income dynamics in Ukraine that limit growth potential for B2C-oriented organizations, 2) lack of financial sector infrastructure, especially in the smaller towns and villages and 3) "trust crisis" by the Ukrainians to financial services following liquidations of a large number of banks. Development of B2C solutions also requires significant investments into wide-scale marketing compared to B2B offerings, which the majority of the FinTech projects typically cannot afford given the overall lack of capital.

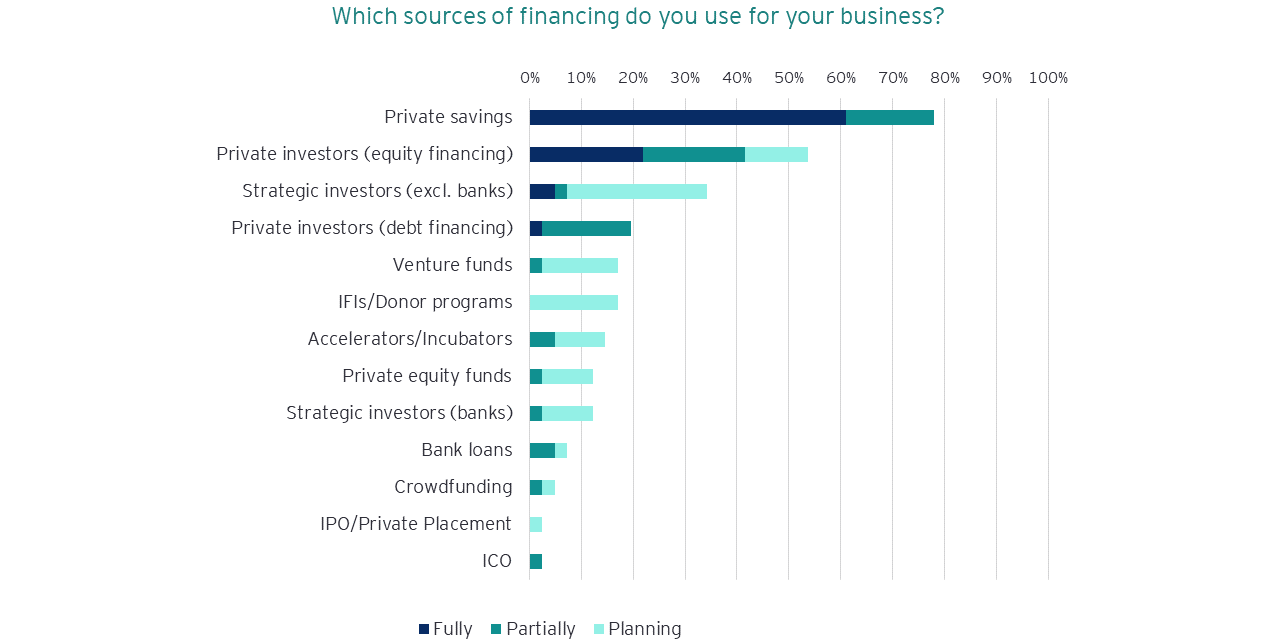

Financing remains an issue for new technology businesses in Ukraine. A significant number of respondents, namely 61%, are fully self-financed. Private equity and debt investors are two other material sources of funding, followed by strategic investors (excl. banks), accelerators/incubators and commercial loans.

97.6% of the respondents said they do not have banks, banking groups, bank-managed corporate accelerators or other bank-affiliated entities in their shareholding structure.

97.6% of the respondents said they do not have banks, banking groups, bank-managed corporate accelerators or other bank-affiliated entities in their shareholding structure.

New tech-based projects globally are typically financed by third-party capital. 61% being fully self-financed in Ukraine shows an overall lack of external capital for development which is slowing down the sector – accordingly, rapid expansion is unlikely. Foreign investors are being very cautious, and none of the traditional commercial banks are offering meaningful loan programs and terms to high-tech development stage businesses.

Operational and opinion insights

For ease of reading and comparison, we have grouped related Operational and Opinion response results together:

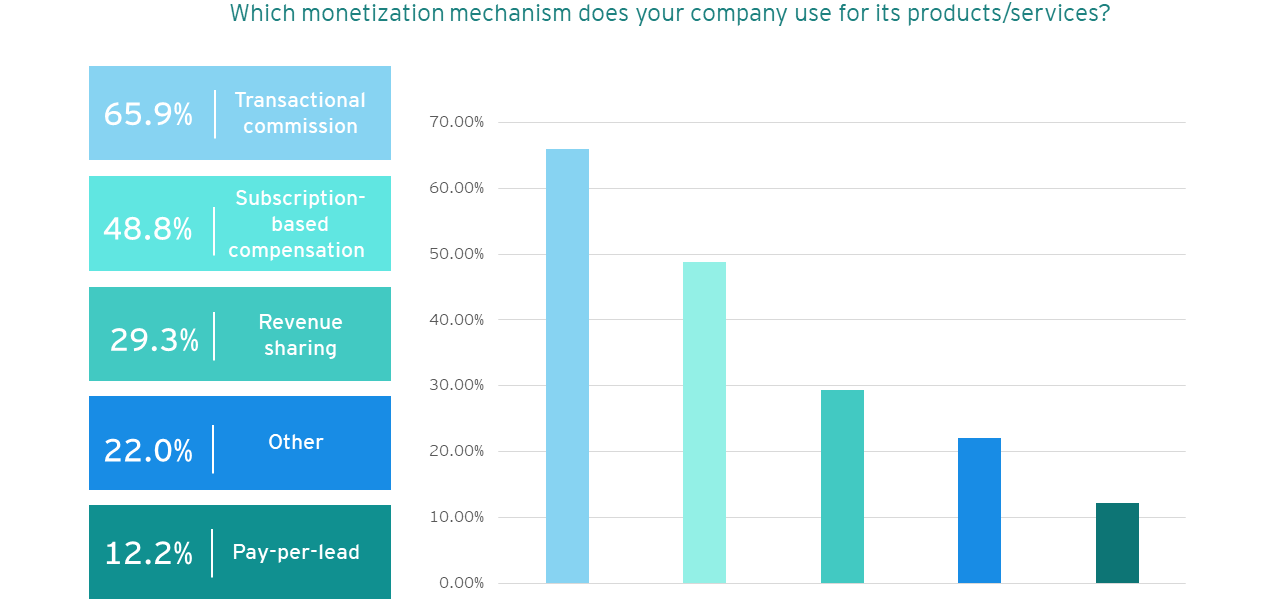

Monetization mechanisms

The most popular way of monetization for the FinTech organizations operating in Ukraine was found to be transactional commission, with 65.9% of the respondents employing this approach. At that, 70.6% of the respondents employ a combination of monetization mechanisms for different clients rather than just one.

However, among those that provide services and solutions to banks, the importance of subscription and revenue sharing mechanisms is much higher – transactional commission model is being employed by 68.4%, subscription-based models are used by 63.2% and revenue sharing is implemented by 57.9% of the respondents cooperating with banks.

«Other» is an option that asked respondents to name their own monetization approach. Specific answers included: "brokerage commission", "royalties", "payment for service and/or product", "license fee".

Monetization mechanisms

The most popular way of monetization for the FinTech organizations operating in Ukraine was found to be transactional commission, with 65.9% of the respondents employing this approach. At that, 70.6% of the respondents employ a combination of monetization mechanisms for different clients rather than just one.

However, among those that provide services and solutions to banks, the importance of subscription and revenue sharing mechanisms is much higher – transactional commission model is being employed by 68.4%, subscription-based models are used by 63.2% and revenue sharing is implemented by 57.9% of the respondents cooperating with banks.

«Other» is an option that asked respondents to name their own monetization approach. Specific answers included: "brokerage commission", "royalties", "payment for service and/or product", "license fee".

Competitiveness

Despite the overall public perception that finding pilot clients for new FinTech solutions is a challenge, 75% of the corporate-oriented respondents required less than 6 months to find their first pilot corporate client after finalizing product development of their solution. Importantly, among those who offer services and solutions to banks, the result is very similar (73.6%).

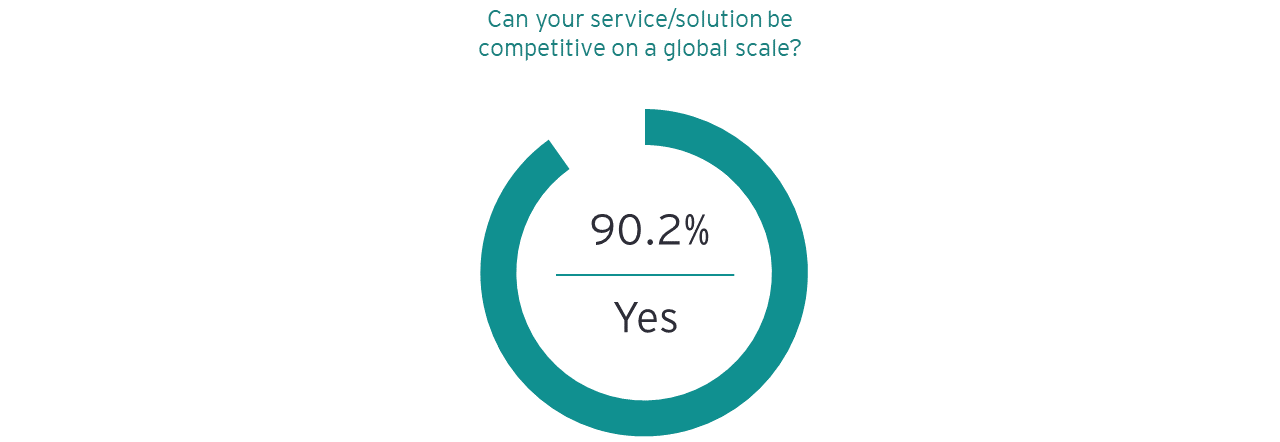

61% of the respondents believe they have less than 5 competitors in their specific niche on the Ukrainian market.

The 'number of competitors' results are expected, given the overall low number of FinTech solutions operating in Ukraine and high barriers to entry. The 'global competitiveness' sentiment, however, is a display of overconfidence and lack of realistic understanding of what global markets have to offer. This 'technological arrogance' may be one of the reasons investors are overlooking many of the Ukrainian-sourced FinTech projects.

Despite the overall public perception that finding pilot clients for new FinTech solutions is a challenge, 75% of the corporate-oriented respondents required less than 6 months to find their first pilot corporate client after finalizing product development of their solution. Importantly, among those who offer services and solutions to banks, the result is very similar (73.6%).

61% of the respondents believe they have less than 5 competitors in their specific niche on the Ukrainian market.

The 'number of competitors' results are expected, given the overall low number of FinTech solutions operating in Ukraine and high barriers to entry. The 'global competitiveness' sentiment, however, is a display of overconfidence and lack of realistic understanding of what global markets have to offer. This 'technological arrogance' may be one of the reasons investors are overlooking many of the Ukrainian-sourced FinTech projects.

Barriers to development and desired legal changes

For several of the "Opinion" questions on the survey, the participants were asked to grade an importance of an issue or a subject in their view from 1 to 5, where 1 meant minimum importance and 5 – maximum importance. This has provided us with a graded sentiment distribution. Accordingly, we have used proprietary methodology to calculate a Weighted Sentiment Index (WSI) on each such question. We normalized the indices, so that they fit into a scale from -100% to 100%, where -100% means the ultimate respondent consensus of non-importance and 100% means ultimate respondent consensus of importance.

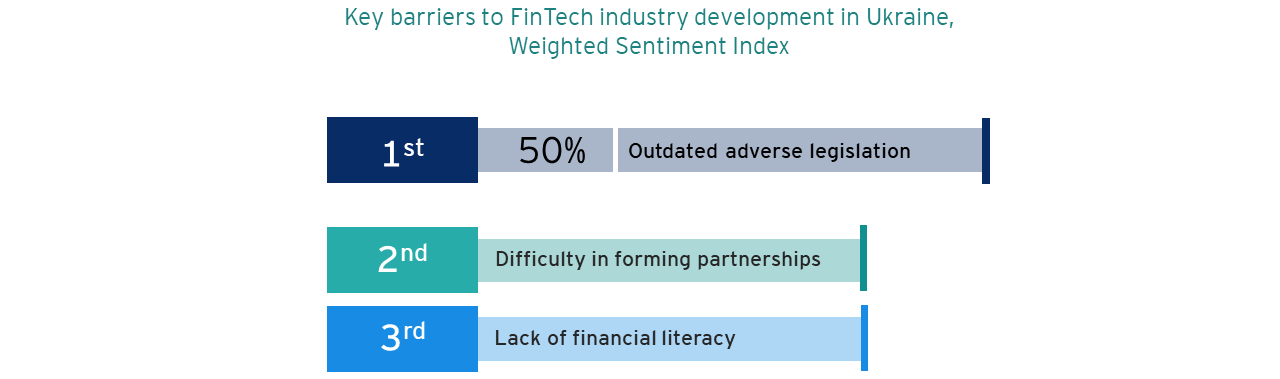

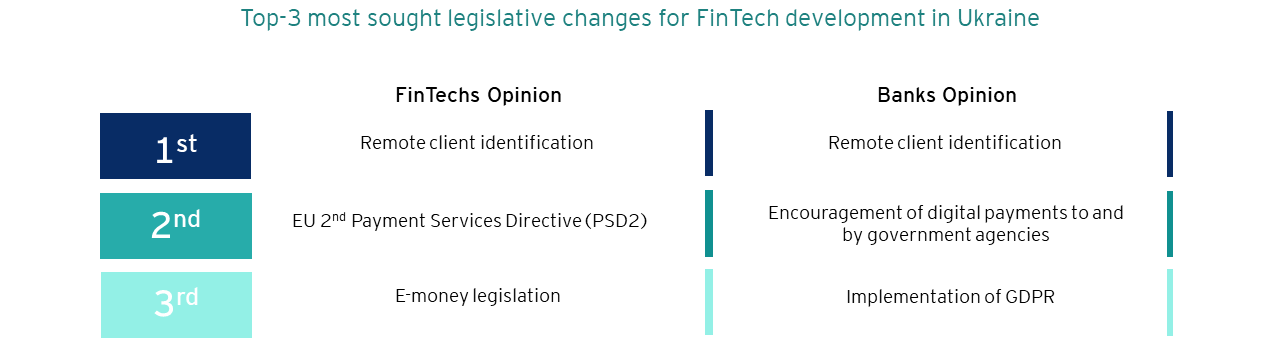

When asked about the key barriers to FinTech development in Ukraine, the highest WSI value - 50% - was attained by outdated adverse legislation. Difficulty in forming partnerships and lack of financial literacy took second and third place as impediments for development.

In terms of legislation, introduction of legal framework for remote client identification and introduction of PSD2 rules were deemed as the most critically sought changes, with a WSI of 62.25% and 52.45%, respectively.

In another insight, 61% of the respondents said they believe liberalization of the foreign exchange market in Ukraine created opportunities for development of new FinTech services.

When asked about the key barriers to FinTech development in Ukraine, the highest WSI value - 50% - was attained by outdated adverse legislation. Difficulty in forming partnerships and lack of financial literacy took second and third place as impediments for development.

In terms of legislation, introduction of legal framework for remote client identification and introduction of PSD2 rules were deemed as the most critically sought changes, with a WSI of 62.25% and 52.45%, respectively.

In another insight, 61% of the respondents said they believe liberalization of the foreign exchange market in Ukraine created opportunities for development of new FinTech services.

Cooperation with banks

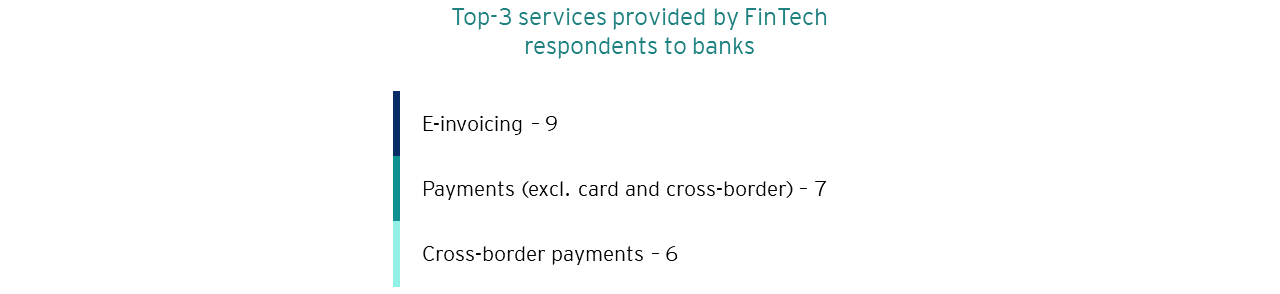

Overall, the respondents have medium exposure to banks as corporate clients, with 46.3% of the respondents providing at least one service or product to a bank. The most popular services provided to banks were e-invoicing (22% of the respondents), other payment types excluding card and cross-border payments (17%) and cross-border payments (14.6%). Crowdfunding, asset management and retail origination services are not provided by FinTech organizations to banks at all.

Overall, the respondents have medium exposure to banks as corporate clients, with 46.3% of the respondents providing at least one service or product to a bank. The most popular services provided to banks were e-invoicing (22% of the respondents), other payment types excluding card and cross-border payments (17%) and cross-border payments (14.6%). Crowdfunding, asset management and retail origination services are not provided by FinTech organizations to banks at all.

While e-money is a top-5 service across all business models, only 12.2% of the respondents issue e-money together with banks. Given that currently only banks are legally allowed to issue e-money in Ukraine, this result conjures questions in regards to the definition of e-money by the market.

Despite the number of respondents cooperating with banks, the majority of respondents - 60.8% - confirmed they frequently experience reluctance of the traditional banking system to embrace new technologies developed by FinTech organizations.

Despite the number of respondents cooperating with banks, the majority of respondents - 60.8% - confirmed they frequently experience reluctance of the traditional banking system to embrace new technologies developed by FinTech organizations.

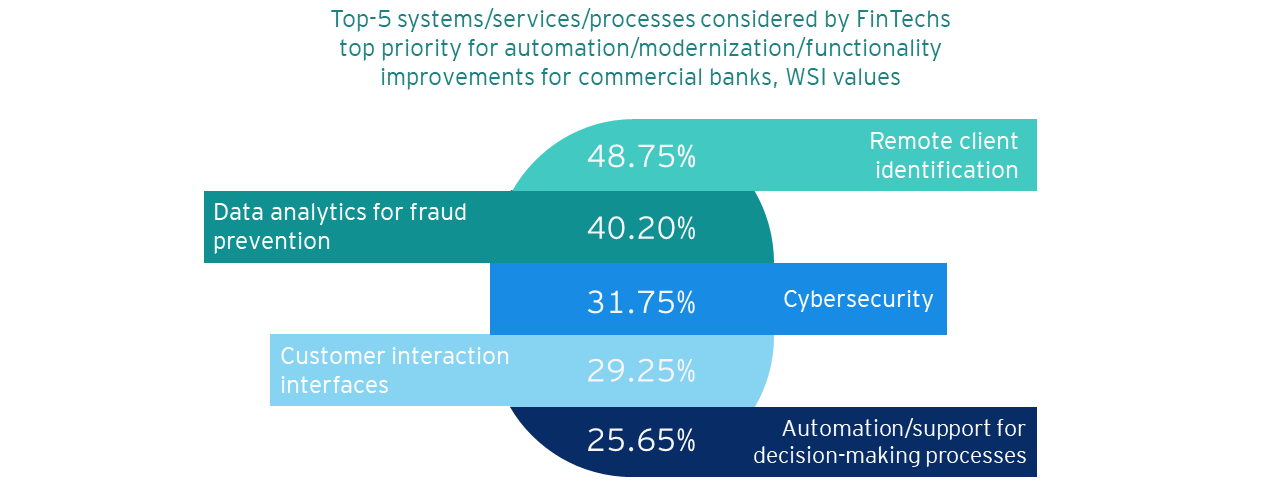

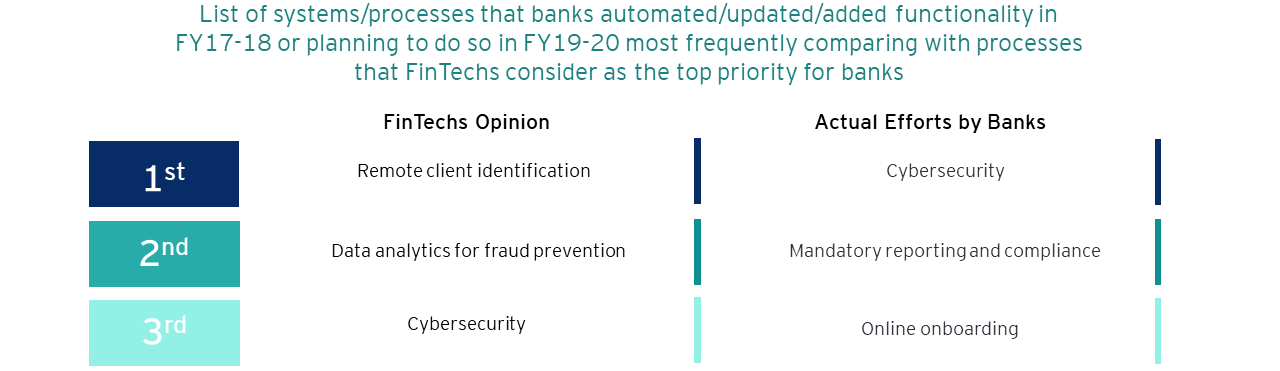

The respondents were asked to provide an opinion on which systems/services/processes are top priority for automation/modernization/functionality improvements for commercial banks. Remote client identification was deemed the most important with a WSI of 48.75%, with data analytics for fraud prevention being another important area of potential focus. At that, modernization of custodial functions was considered the lowest priority for banks with a WSI of -67.05%.

Among those who provide services and solutions to banks, the top-5 remained the same, although with a change of order between spots #3, 4 and 5.

Among those who provide services and solutions to banks, the top-5 remained the same, although with a change of order between spots #3, 4 and 5.

New FinTech solutions

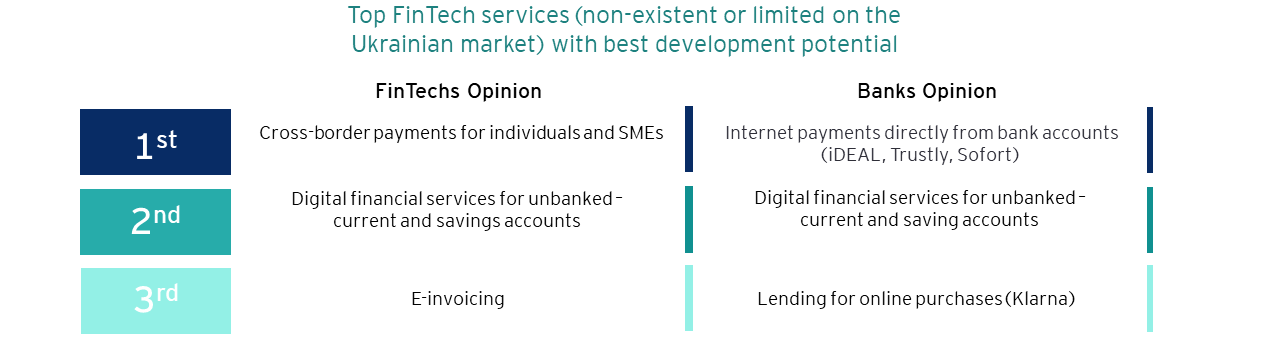

When asked to grade FinTech services that are non-existent or barely introduced in Ukraine for their development potential, cross-border payments for SMEs and individuals lead the consensus with a WSI of 32.9%. Cross-border investment applications were considered the least interesting niche for development of new projects.

When asked about the most popular revolutionary FinTech service/business models currently missing in Ukraine, the most frequent responses were PayPal, P2P loans and cryptocurrency operations.

To that end, we also asked the respondents about what they considered the most important FinTech development on the Ukrainian market last year. 50% of those who answered – the question was optional - stated the full-scale launch of Monobank.

When asked to grade FinTech services that are non-existent or barely introduced in Ukraine for their development potential, cross-border payments for SMEs and individuals lead the consensus with a WSI of 32.9%. Cross-border investment applications were considered the least interesting niche for development of new projects.

When asked about the most popular revolutionary FinTech service/business models currently missing in Ukraine, the most frequent responses were PayPal, P2P loans and cryptocurrency operations.

To that end, we also asked the respondents about what they considered the most important FinTech development on the Ukrainian market last year. 50% of those who answered – the question was optional - stated the full-scale launch of Monobank.

NBU innovations hub

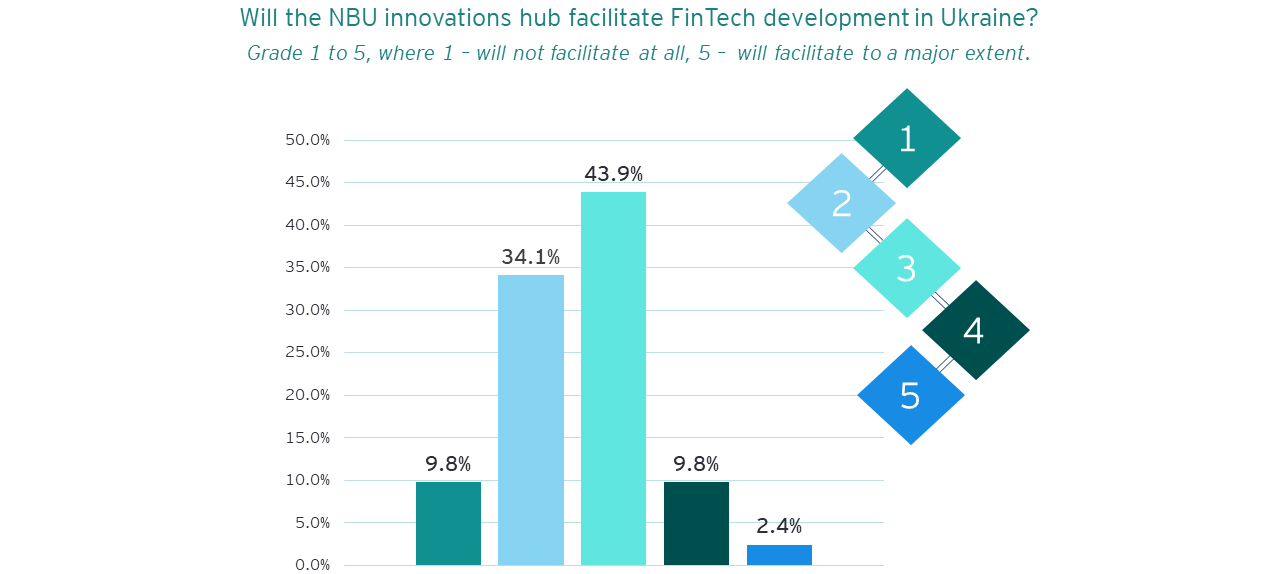

The respondents were asked whether they believe the NBU innovations hub will facilitate FinTech development in Ukraine. With a WSI of -19.55% (-15.79% among those who provide services and solutions to banks), the FinTech community's expectations for the NBU hub's performance and usefulness seem to be quite low. This may be caused by a misunderstanding of the role of such a Center and the mechanisms of its interaction with other stakeholders within the local market.

The respondents indicated the importance of setting up the working groups on the priority topics with the key market players, as well as the ability to work in the "sandbox" under the regulator's supervision, and to introduce pilot solutions. FinTech companies want to see real help with the advancement of technologies, software and services.

FinTech companies also stated that they would like to see the Hub as: an open platform for the dialogue of traditional and new players of the FinTech industry, a consulting center, a place for events for the key market players, a place that would be open "to hear" the real needs of the market and initiate necessary legislative changes for its development.

The respondents were asked whether they believe the NBU innovations hub will facilitate FinTech development in Ukraine. With a WSI of -19.55% (-15.79% among those who provide services and solutions to banks), the FinTech community's expectations for the NBU hub's performance and usefulness seem to be quite low. This may be caused by a misunderstanding of the role of such a Center and the mechanisms of its interaction with other stakeholders within the local market.

The respondents indicated the importance of setting up the working groups on the priority topics with the key market players, as well as the ability to work in the "sandbox" under the regulator's supervision, and to introduce pilot solutions. FinTech companies want to see real help with the advancement of technologies, software and services.

FinTech companies also stated that they would like to see the Hub as: an open platform for the dialogue of traditional and new players of the FinTech industry, a consulting center, a place for events for the key market players, a place that would be open "to hear" the real needs of the market and initiate necessary legislative changes for its development.

KEY FINDINGS – BANK RESPONDENTS

Profiling

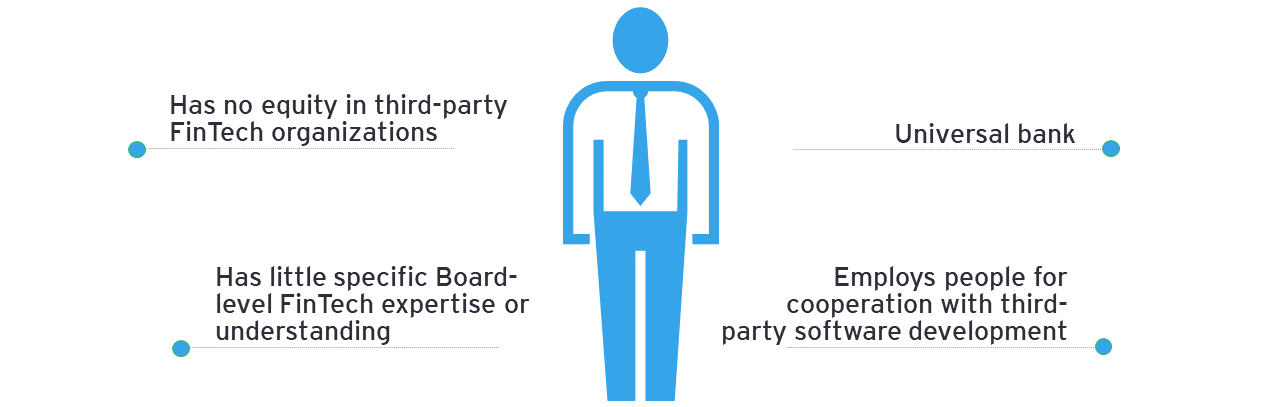

Similar to FinTech, we compiled a summary profile of an average Bank respondent. Our average respondent is a universal bank that employs people specifically dedicated to cooperation with third-party software providers but has little FinTech expertise or understanding at Board level. Accordingly, the typical responding bank does not own or invest in third-party FinTech companies.

Average Bank respondent profile:

Average Bank respondent profile:

The numbers:

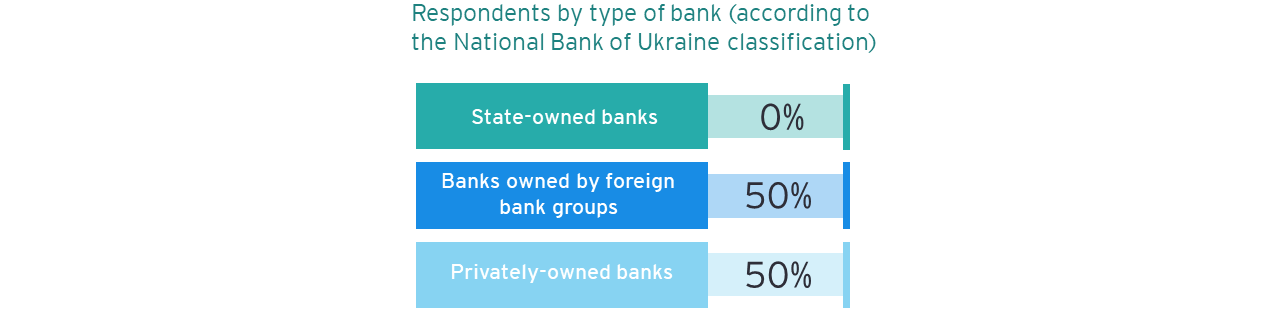

50% of the respondents are banks with foreign capital, while the other 50% are banks with Ukrainian capital. Unfortunately, none of the state-owned banks completed the survey.

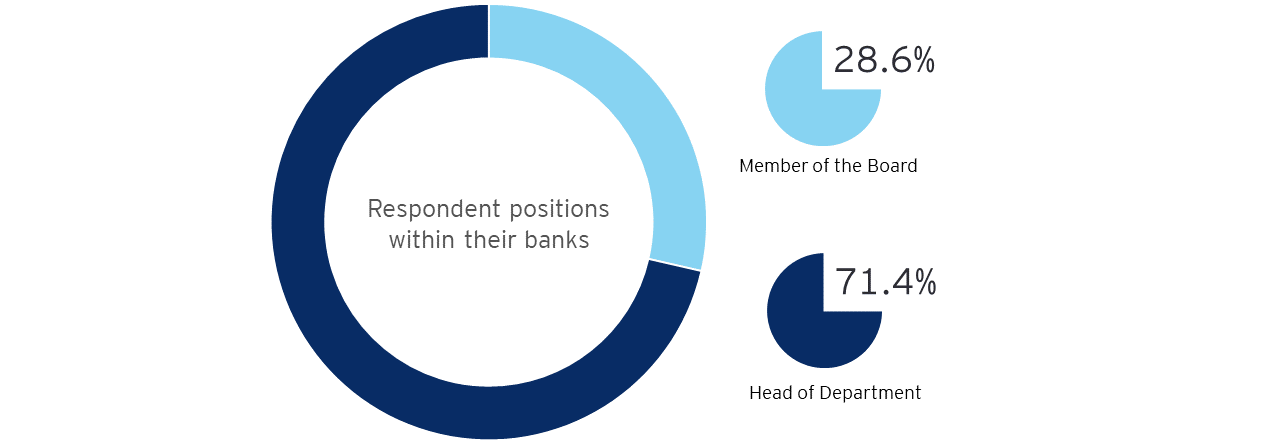

100% of the bank representatives filling out the survey were either Members of the Board or Heads of Department (Risks, Digital, Financial, Operations).

64.3% of the respondents are universal banks, with another 14.3% being corporate-focused banks.

85.7% of the responding banks (or their affiliated entities) do not hold equity in FinTech organizations.

78.6% of the respondents employ people dedicated to cooperation with software development companies and the FinTech sector. Yet, just 50% have people dedicated to digital strategy and transformation and 35.7% employ experts specifically responsible for identification and unlocking potential of the FinTech sector.

71.4% of the respondents do not have a single Board Member with expertise in FinTech or digital strategy and transformation.

100% of the bank representatives filling out the survey were either Members of the Board or Heads of Department (Risks, Digital, Financial, Operations).

64.3% of the respondents are universal banks, with another 14.3% being corporate-focused banks.

85.7% of the responding banks (or their affiliated entities) do not hold equity in FinTech organizations.

78.6% of the respondents employ people dedicated to cooperation with software development companies and the FinTech sector. Yet, just 50% have people dedicated to digital strategy and transformation and 35.7% employ experts specifically responsible for identification and unlocking potential of the FinTech sector.

71.4% of the respondents do not have a single Board Member with expertise in FinTech or digital strategy and transformation.

Operational Insights

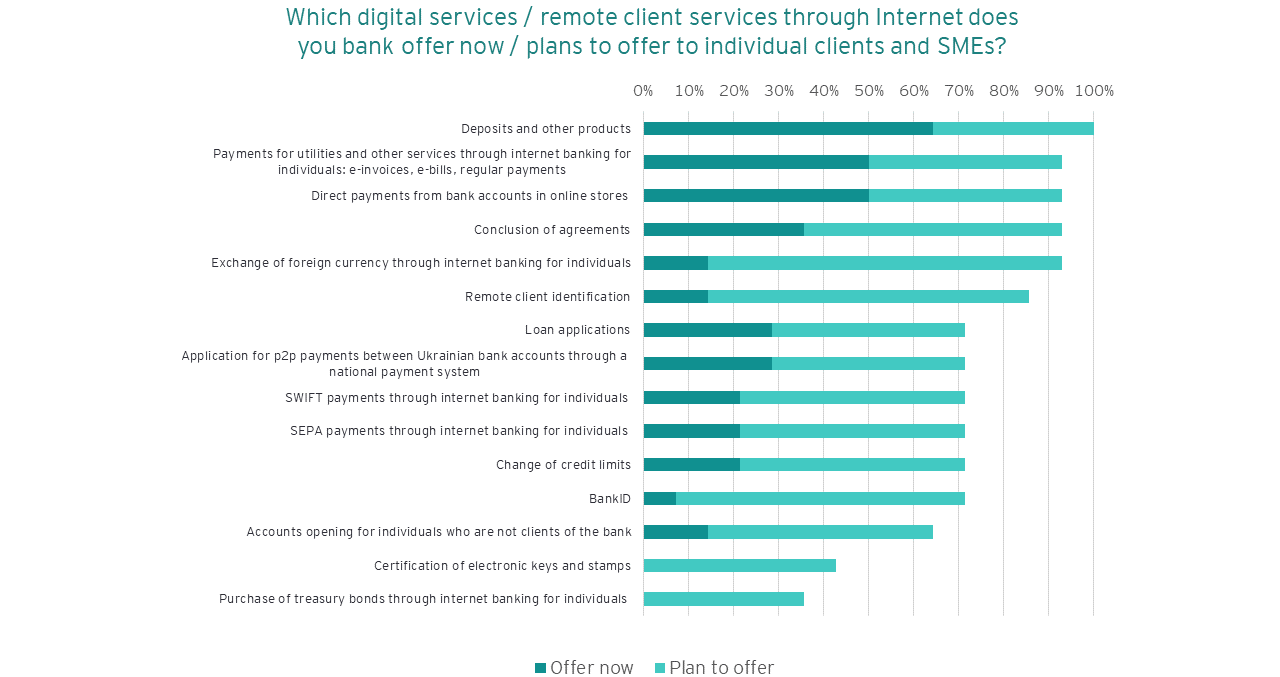

Commercial banks in Ukraine generally follow the mass market demand trend when devising and launching digitalized services for customers. Accordingly, the most popular digital/remote customer services offered by the banks to retail and SME segments are focused on the day-to-day needs of the target audience.

100% of the respondents said they are providing or planning to provide deposits and other products remotely. Other "popular" digital services mentioned by the respondents were Internet banking-based payments for utilities and other services for individuals, online conclusion of contracts, foreign currency exchange for individuals as part of online banking services and direct payments from bank accounts in online stores.

The appearance of the last option (direct payments from bank accounts in online stores) in the Top-5, however, should be viewed cautiously. This service is nonexistent in Ukraine today and to create it, a partnership of several big banks and significant investments are needed. Accordingly, given the number of 'offer now' answers, the respondents may either have misunderstood the question or have it on their 'wish lists' rather than in immediate implementation plans.

The least popular services on the list were certification of electronic keys and stamps and purchase of treasury bonds by individuals through internet banking capacities – none of the respondents are offering those services now, though circa 40% are planning to do so in the future.

100% of the respondents said they are providing or planning to provide deposits and other products remotely. Other "popular" digital services mentioned by the respondents were Internet banking-based payments for utilities and other services for individuals, online conclusion of contracts, foreign currency exchange for individuals as part of online banking services and direct payments from bank accounts in online stores.

The appearance of the last option (direct payments from bank accounts in online stores) in the Top-5, however, should be viewed cautiously. This service is nonexistent in Ukraine today and to create it, a partnership of several big banks and significant investments are needed. Accordingly, given the number of 'offer now' answers, the respondents may either have misunderstood the question or have it on their 'wish lists' rather than in immediate implementation plans.

The least popular services on the list were certification of electronic keys and stamps and purchase of treasury bonds by individuals through internet banking capacities – none of the respondents are offering those services now, though circa 40% are planning to do so in the future.

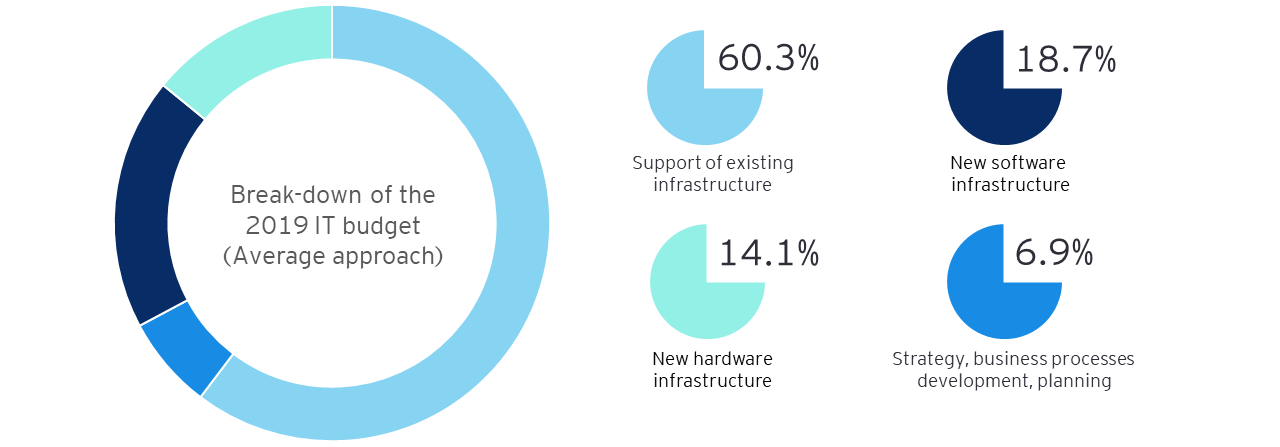

On average, 60.3% of the respondents' IT budget for 2019 is directed towards support of existing infrastructure with just 18.7% devoted to investments in new software infrastructure.

Global data on breakdown of IT budgets between support of legacy systems and investments into new capabilities is hard to find. However, there is an expert consensus that for mid-sized banks, investment into 'strategic technologies' falls within the range of 25-35% of the overall IT budgets. The results of our survey are then more or less in line with the global trend.

What is definitely against the trend is the fact that most of the IT work is being done using internal resources of the banks – especially in the strategy and planning improvements area, which globally is typically referred to third-party support.

Global data on breakdown of IT budgets between support of legacy systems and investments into new capabilities is hard to find. However, there is an expert consensus that for mid-sized banks, investment into 'strategic technologies' falls within the range of 25-35% of the overall IT budgets. The results of our survey are then more or less in line with the global trend.

What is definitely against the trend is the fact that most of the IT work is being done using internal resources of the banks – especially in the strategy and planning improvements area, which globally is typically referred to third-party support.

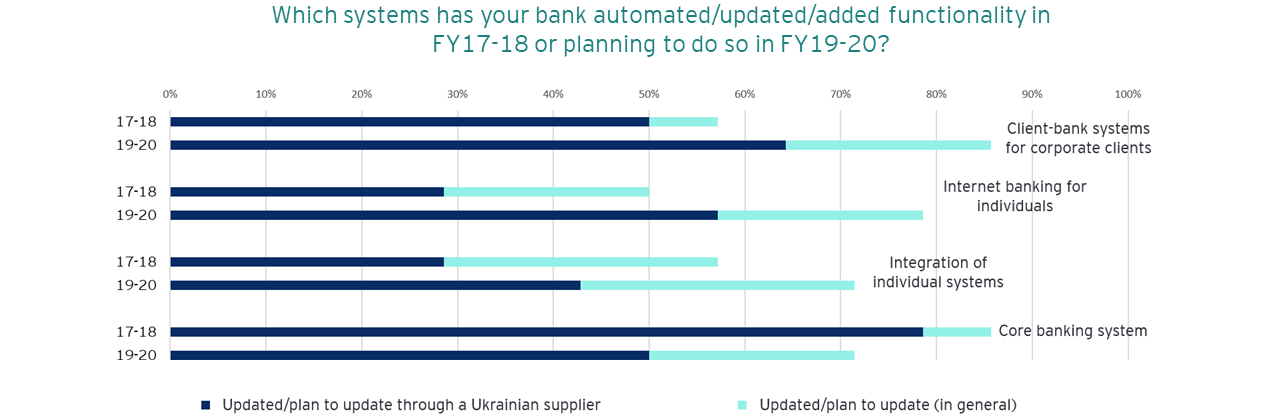

The key bank IT systems that were (FY2018) or are (FY2019) the focus of modernization and update include client-bank systems for corporate customers, online banking for individuals, core banking systems, mobile banking and integration of individual systems. Over 70% of the respondents indicated these systems have undergone modernization (or will in the near future). E-wallet was of low interest, with only a third of respondents invested or planning to invest into the function this financial year.

Strategy, business processes development, support of existing infrastructure and introduction of new hardware are predominantly performed using internal resources of the banks, while introduction of new software is split 50/50 between internal resources and third-party providers.

Internal modernization or update of services and processes is focused predominantly on the following areas: cybersecurity, mandatory reporting and compliance, online applications for financial products, data analytics for fraud prevention, management accounting and sales improvements. Investment into these categories has been or is planned in the near future at over 70% of the respondents.

Strategy, business processes development, support of existing infrastructure and introduction of new hardware are predominantly performed using internal resources of the banks, while introduction of new software is split 50/50 between internal resources and third-party providers.

Internal modernization or update of services and processes is focused predominantly on the following areas: cybersecurity, mandatory reporting and compliance, online applications for financial products, data analytics for fraud prevention, management accounting and sales improvements. Investment into these categories has been or is planned in the near future at over 70% of the respondents.

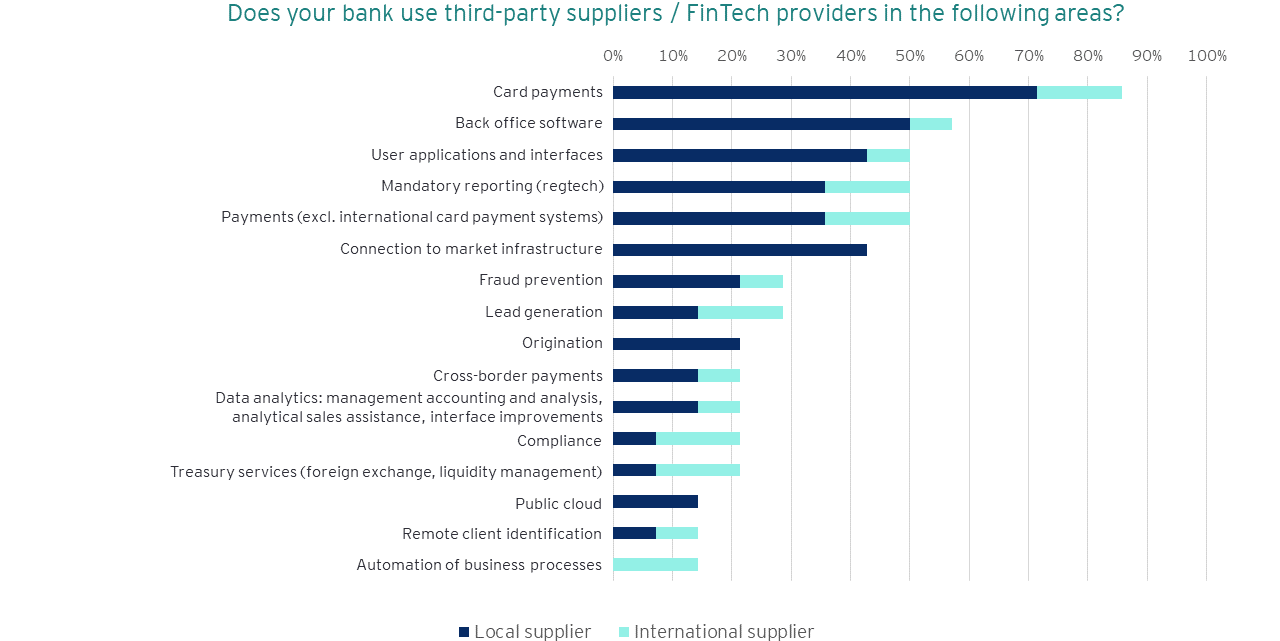

Cooperation with FinTech solution providers is limited. Card payments is the only third-party service that is systemically in demand by the banks- with 85.7% of the respondents cooperating with third-party providers (71.4% of them are using local providers). Back office software development and maintenance is being done by third-party providers at 57.1% of respondents. Management of business processes is the least outsourced solution with only 14.3% of the respondents engaging third-party providers (and none of those providers are local).

None of the responding banks issue e-money. At that, 42.9% of the respondents offer e-wallet services, but all of the offerings are international brands (Apple Pay, Android Pay).

Interestingly enough, while globally the traditional financial services sector players pay increasingly close attention to practical applications of distributed ledger technologies (blockchain tech being the most well-known), none of the respondents in our survey are using or planning to implement DLT solutions.

Use of cloud solutions is very limited. Less than 10% of the respondents keep over 40% of their services in either private or public cloud, with an absolute majority keeping from 0% to 20% of the services in the cloud.

Interestingly enough, while globally the traditional financial services sector players pay increasingly close attention to practical applications of distributed ledger technologies (blockchain tech being the most well-known), none of the respondents in our survey are using or planning to implement DLT solutions.

Use of cloud solutions is very limited. Less than 10% of the respondents keep over 40% of their services in either private or public cloud, with an absolute majority keeping from 0% to 20% of the services in the cloud.

Opinion insights

Similar to the FinTech survey, we used the WSI approach on several "Opinion" questions in the Banks survey.

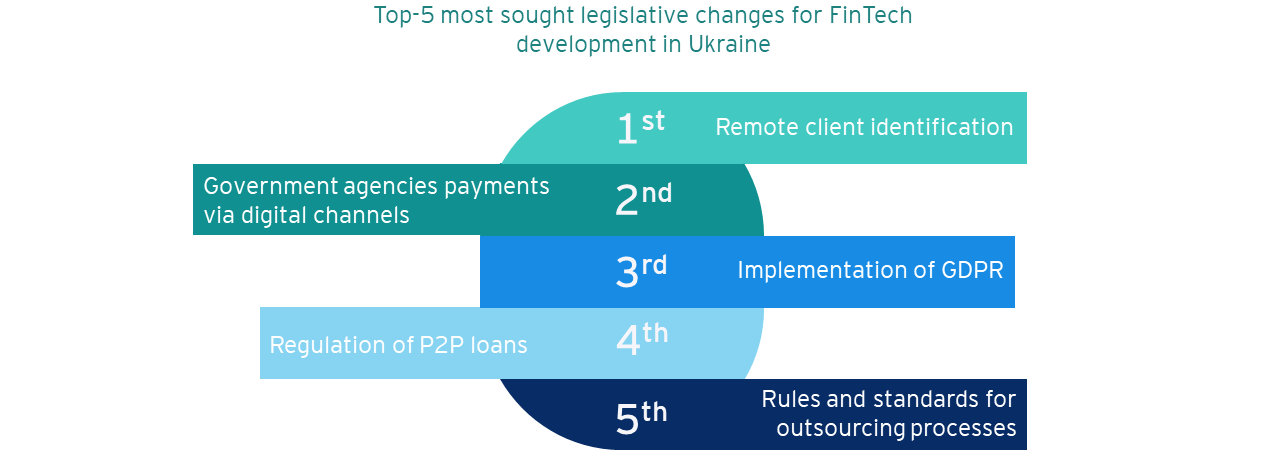

The respondents were asked to provide an opinion on the most critical legislative changes required for development of the FinTech sector in Ukraine. Introduction of legal framework for remote client identification and encouragement of payments by and to government agencies through digital channels were deemed the most important with a WSI of 35.8% and 17.85%, respectively.

85.7% of the respondents saying they believe liberalization of the foreign exchange market in Ukraine created opportunities for development of new FinTech services.

The respondents were asked to provide an opinion on the most critical legislative changes required for development of the FinTech sector in Ukraine. Introduction of legal framework for remote client identification and encouragement of payments by and to government agencies through digital channels were deemed the most important with a WSI of 35.8% and 17.85%, respectively.

85.7% of the respondents saying they believe liberalization of the foreign exchange market in Ukraine created opportunities for development of new FinTech services.

Key challenges

When asked to grade FinTech services that are non-existent or limited on the Ukrainian market for their development potential, none of the options provided to respondents for grading gained any positive consensus, with WSI values for all the options being below 0%. At that, the most positive weighted reaction was attained by the online credit transfer services (systems similar to iDEAL, Trustly, Sofort et al.).

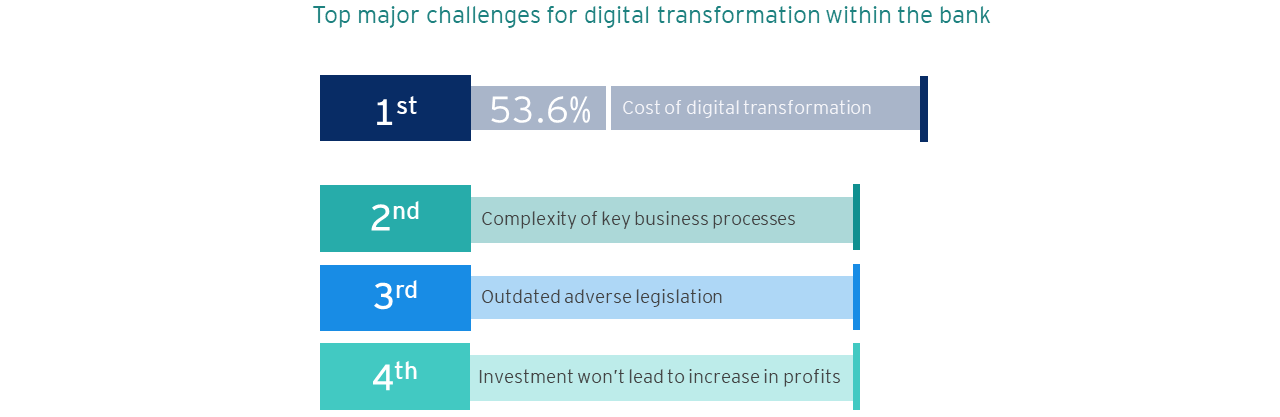

The respondents were also asked about their opinion on the biggest challenges to digital transformation for their bank. Cost of digital transformation was an undoubted winner with a WSI value of 53.6%. All other options have shown no consensus, with the WSI values being below 0%. Of these, complexity of key business processes has the highest WSI value. Importantly, the option 'No demand for digital transformation by shareholders and/or management' was almost unanimously seen as the least of the challenges.

The respondents were also asked about their opinion on the biggest challenges to digital transformation for their bank. Cost of digital transformation was an undoubted winner with a WSI value of 53.6%. All other options have shown no consensus, with the WSI values being below 0%. Of these, complexity of key business processes has the highest WSI value. Importantly, the option 'No demand for digital transformation by shareholders and/or management' was almost unanimously seen as the least of the challenges.

FinTech sector perception

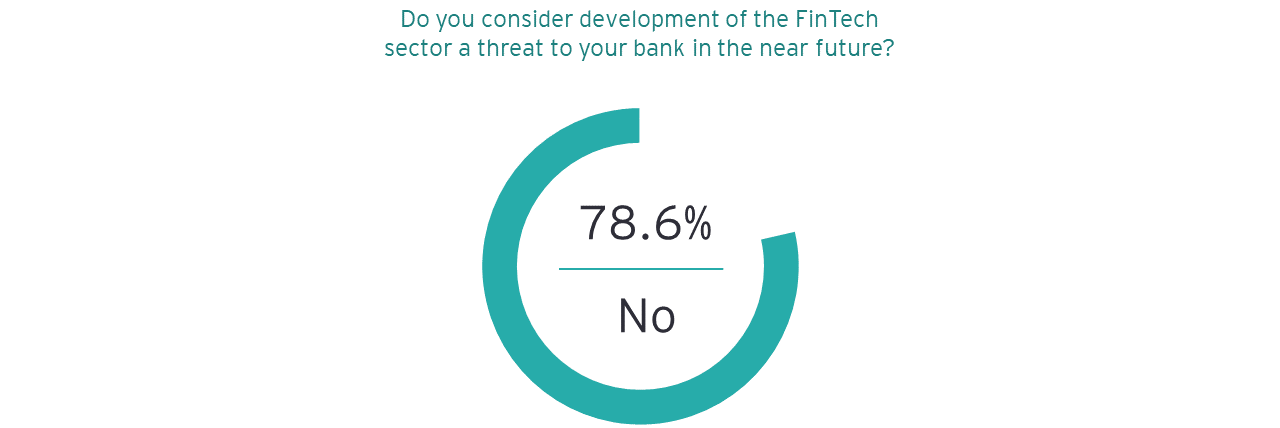

78.6% of the respondents do not view the FinTech sector as a threat to their bank. Some respondents, who believe FinTech advancements could pose a threat to their bank in the near future, mentioned that traditional banks may be unable to compete with FinTech players due to more stringent regulatory requirements for banks.

The result of 'is FinTech a threat' question suggests that banks in Ukraine tend to underestimate new trends and the innovation culture. As mentioned in the Global Trends section of the report, 88% of global financial service providers do believe their market share is under pressure from FinTech innovators and are looking at opportunities to incorporate those innovations into their own businesses. Ukrainian banks, on the contrary, with a few notable exceptions, neither understand the threat, nor have the strategies in place to deal with it.

The result of 'is FinTech a threat' question suggests that banks in Ukraine tend to underestimate new trends and the innovation culture. As mentioned in the Global Trends section of the report, 88% of global financial service providers do believe their market share is under pressure from FinTech innovators and are looking at opportunities to incorporate those innovations into their own businesses. Ukrainian banks, on the contrary, with a few notable exceptions, neither understand the threat, nor have the strategies in place to deal with it.

COMPARISON OF THE RESULTS

The difference between FinTech and Bank respondents on the issues raised within this survey is striking, given that they are all part of the same Ukrainian financial services universe. This may partially be attributed to a large number of FinTech organizations operating both in and outside of Ukraine and being exposed to global drivers, which are not felt so acutely within Ukraine.

Importantly, both FinTechs and banks see the need for enabling remote client identification, as the most necessary legislative change required.

Finally, and maybe most importantly, both FinTechs and banks see major potential in future projects focused on financial services for the unbanked – a lucrative niche for new FinTech offerings both from new players and incumbents.

At that, unfortunately, development of applications for cross-border investments is not interesting for either respondent group – meaning the FinTech market and the demand trends in Ukraine are still far from a developed stage.

Finally, and maybe most importantly, both FinTechs and banks see major potential in future projects focused on financial services for the unbanked – a lucrative niche for new FinTech offerings both from new players and incumbents.

At that, unfortunately, development of applications for cross-border investments is not interesting for either respondent group – meaning the FinTech market and the demand trends in Ukraine are still far from a developed stage.

© 1999-2019 AIN.UA

При использовании материалов сайта обязательным условием является наличие гиперссылки в пределах первого абзаца на страницу расположения исходной статьи с указанием бренда издания AIN.UA. Материалы с пометками «Новости компаний» и PR публикуются на правах рекламы.

При использовании материалов сайта обязательным условием является наличие гиперссылки в пределах первого абзаца на страницу расположения исходной статьи с указанием бренда издания AIN.UA. Материалы с пометками «Новости компаний» и PR публикуются на правах рекламы.

ЧИТАТЬ

© 1999-2019 AIN.UA

При использовании материалов сайта обязательным условием является наличие гиперссылки в пределах первого абзаца на страницу расположения исходной статьи с указанием бренда издания AIN.UA. Материалы с пометками «Новости компаний» и PR публикуются на правах рекламы.

При использовании материалов сайта обязательным условием является наличие гиперссылки в пределах первого абзаца на страницу расположения исходной статьи с указанием бренда издания AIN.UA. Материалы с пометками «Новости компаний» и PR публикуются на правах рекламы.

ЧИТАТЬ